The Hidden Costs of Our Contracting Choices – Inside the Industry Contracting Strategies for Capital Projects

One most-often overlooked, though seemingly obvious, element of a successful industrial project is ensuring that every part of the contracting set-up supports not only the project’s unique characteristics and environment but also the unique capabilities of the involved stakeholders, from the owner to various contractors.

Many owner companies generally do not quantify the direct effects of their deals on their office costs when considering growth strategies in an increasingly turbulent market.

Instead, the larger the company’s project portfolio is, the more it gets absorbed in its own contracting tradition, easily neglecting the importance of closely understanding the connections between the industry contracting trends and the company’s deal shaping elements such as scaling, timing, and risk allocation.

Split Form Contracting on the Rise

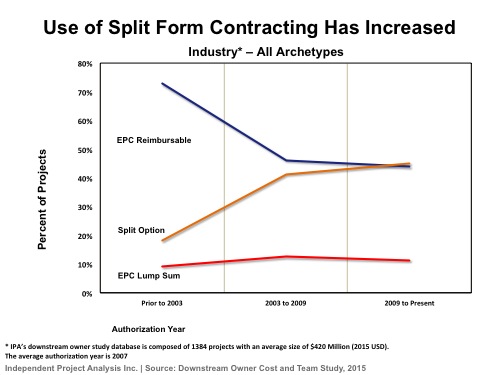

As shown below, split form contracting,1 we found, has recently become the industry’s dominant contracting strategy, leading over the reimbursable engineering, procurement, and construction (EPC reimbursable) form.2 Additionally, based on the largest project global dataset available, we also found that industry projects are most cost effective when using split form contracting.3

Exhibit 1

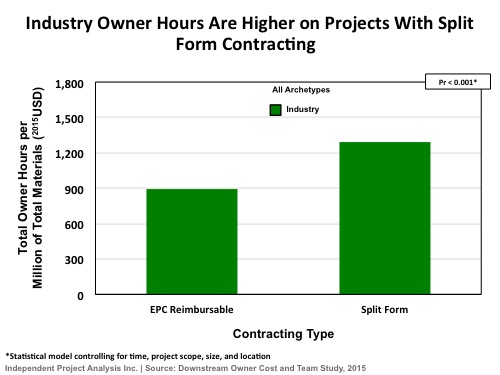

The specific example of international major oil and gas companies still dominantly using an EPC reimbursable contracting strategy across their projects in contrast to the industry trend carries with it many questions on how will these companies adjust to ensure the successful execution of their deals. For instance, project executives should ask themselves if they have enough resources to manage a voluntary, or in many cases market-imposed, shift to split form contracting as the latter requires more owner hours—compared to EPC reimbursable—to manage the interface between engineering and construction contractors.

Exhibit 2

Furthermore, the complexity of such questions increases with the changes in other contracting elements such as sourcing. For instance, over the past 10 years, the overall use of Engineering Value Centers 4 (EVCs) has increased 5 in the pursuit of lowering project costs along with a shortage of available engineers in developed countries. While using EVCs promises achievable benefits provided the right practices are used, our research shows it remains challenging and therefore requires more effort focused on the interface and “set-up,” detailed communication plans, detailed and written documentation, and work sharing discipline across the offices.

Many deals underperform because decision-makers neglect the hidden costs of the un-identified connections between a contracting strategy and the environment the strategy will be executed in, taking a one-size-fits-all approach to their deals without properly assessing the company’s time trends compared to Industry from various unconventional analytical aspects.

To avoid such problems, often, a good place to start is to independently analyze the company’s effectiveness using different contracting strategies in relation to the evolution of its internal project capabilities.

Related Articles

- Despite Risks, Industrial Projects in Emerging Markets Can Be Competitive

- Project Office Costs: The Right Mindset

1 Split Option: Engineering contractor (or contractors in multi-prime situation) who performs engineering and procurement is separate from contractor(s) who perform construction management and/or construction.

2 EPC Reimbursable: Engineering contractor (or contractors in multi-prime situation) performs engineering, procurement, construction management, and/or construction on a reimbursable basis.

3 IPA’s downstream owner study database is composed of 1384 projects with an average size of $420 Million (2015 USD). The average authorization year is 2007.

4 EVCs are engineering offices with hourly rates that are significantly (~$60) lower than more developed regions.

5 Looking at a 10 years of data including 3,250 projects of which 22 percent used EVC; controlling for project size; the median project cost is $121 million.

Contributors to the Downstream Project Office Cost Study Team: Ron Auld, Neal Banks, Lucas Milrod, Alex Ogilve, and Andras Marton

Contributors to the EVC Study Team: Dean Findley and Kate Rohrbaugh

This article is the third of a series of articles depicting several aspects of downstream project office costs. Data used were extracted from IPA’s Downstream Project Office Cost Study, which was performed for one of IPA’s clients. The study characterized time trends in the client and Industry downstream owners costs and staffing, showed where the client was comparable to or different from Industry, identified links to overall project outcomes, and opportunities for the client to improve its project performance through owner staffing strategies. Other data used in this article were extracted from IPA’s study on Engineering Value Centers, presented at IBC 2015.